Executive Summary

Sustained demand from an aging population and interest from institutional investors is likely to lead to above-average returns for the senior housing sector in the current cycle. A positive outlook is supported by the following secular trends:

INTRODUCTIONSenior housing facilities provide healthcare and hospitality services to aging households and are segmented based on resident medical acuity levels and the required level of care: independent living, assisted living, and memory care. The average age of senior housing residents is early-to-mid 80s. While demand for independent care is more discretionary and strongly influenced by the health of the broader economy and housing market, demand for assisted living and memory care is typically event-driven (e.g. physical fall, declining memory, poor diet/health), resulting in the need for assistance with “activities of daily living” (ADLs). While several states offer Medicaid waiver programs that help to offset the cost of support services, Medicaid does not cover the cost of room and board at senior housing facilities. As such, senior housing is privately funded. Consequently, the population growth and health (both financial and physical) of older age cohorts and their adult children are key determinants of demand.

OUTPERFORMANCE ACROSS HISTORICAL REAL ESTATE CYCLES

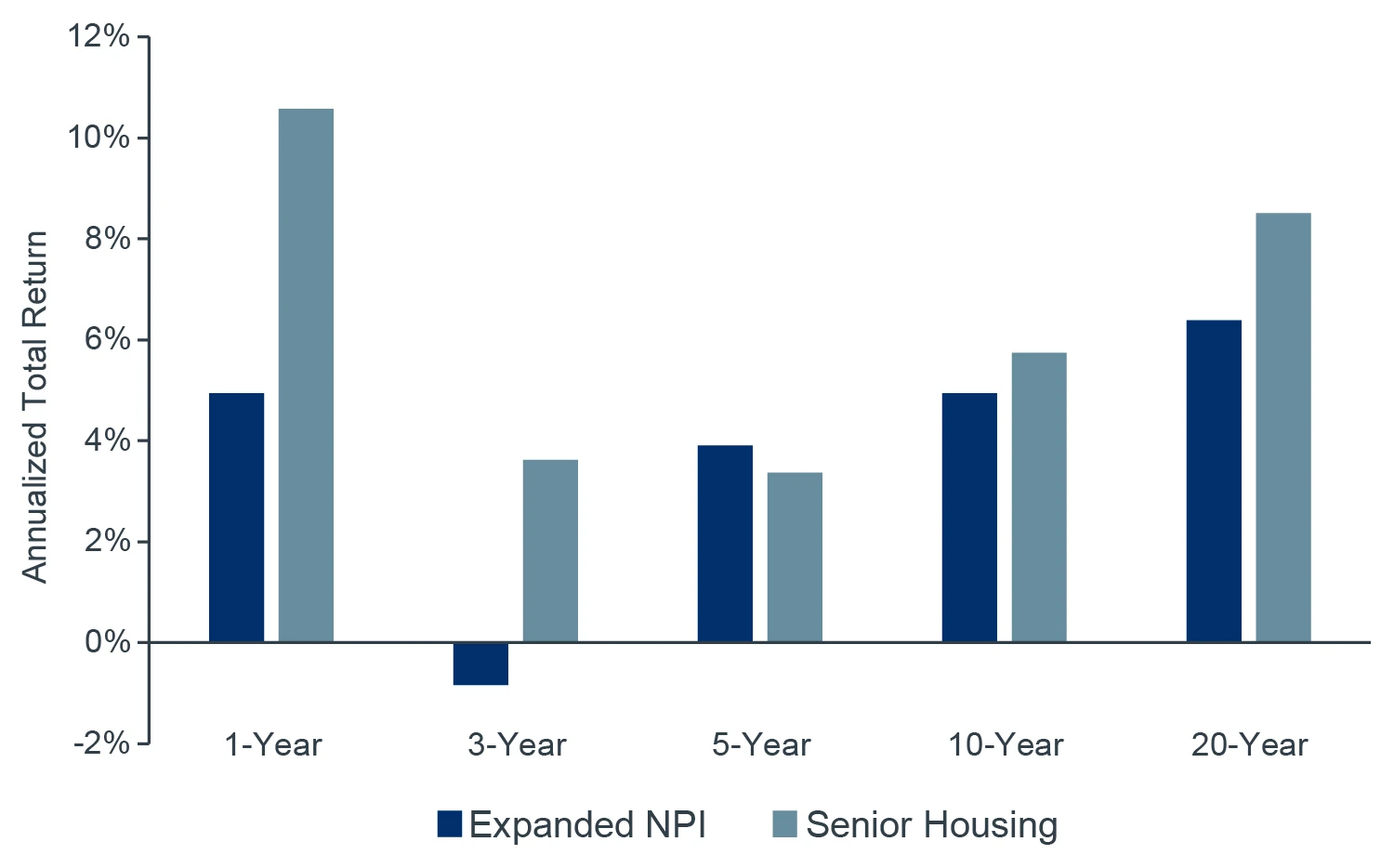

Senior housing has delivered long-term outperformance, with historical total returns exceeding that of the Expanded NCREIF Property Index (NPI) by ~210 bps/year over the last 20 years.1 Notwithstanding the once-in-a-generation negative impact of the COVID pandemic (a significant driving factor behind the sector’s underperformance over the last five years), the less discretionary nature of demand in the sector, particularly for the higher acuity segments of the market, has contributed to its historical outperformance and lower volatility across economic cycles (Figure 1). Outperformance is expected to continue as improving profit margins, driven by rising rental rates and moderating expense growth, contribute to improved NOI growth and valuations.

FIGURE 1: SENIOR HOUSING HAS OUTPERFORMED THE BROADER ALL-PROPERTY INDEX

Source: NCREIF – Expanded NPI, Clarion Partners Global Research, as of 4Q 2025.

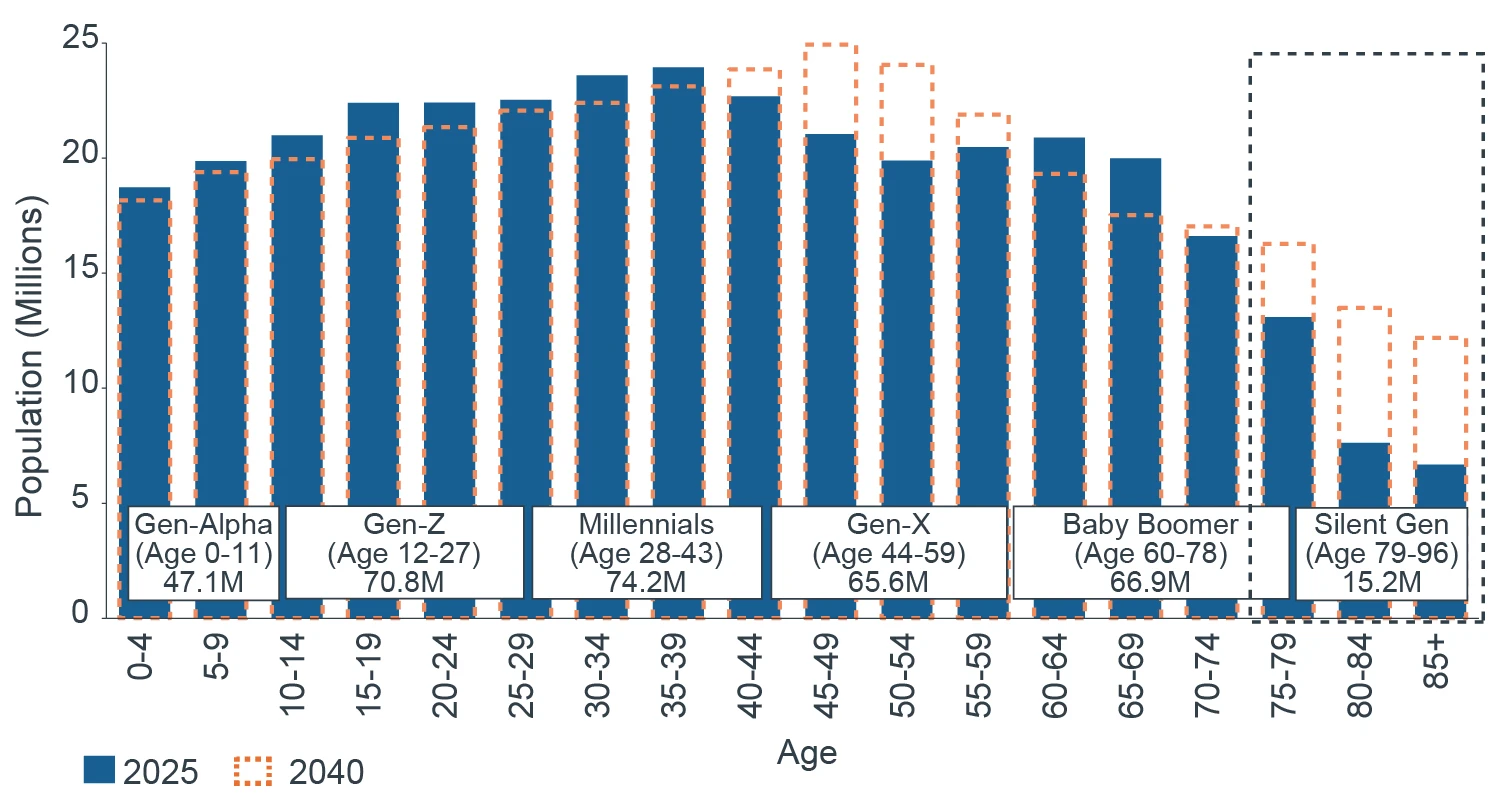

THE LONG-ANTICIPATED "SILVER TSUNAMI" MAKES LANDFALLThe 80+ population is expected to increase at an unprecedented rate over the next two decades, growing at an average annual rate above 4% through 2030 and above 3% well into the 2030s, far outstripping overall population growth2 (Figure 2). As a result, the 80+ population is expected to nearly double by 2040. This demographic tailwind, combined with substantial growth in net worth and improvements in health outcomes among older households today relative to prior generations, should provide a consistent, strong demand tailwind for the sector through the coming decade.

FIGURE 2: AGING BABY BOOMER TAILWIND SHOULD PERSIST INTO THE COMING DECADE

Source: Moody’s Analytics forecast as of January 2026, Clarion Partners Global Research.

PERSISTENT SUPPLY/DEMAND IMBALANCE

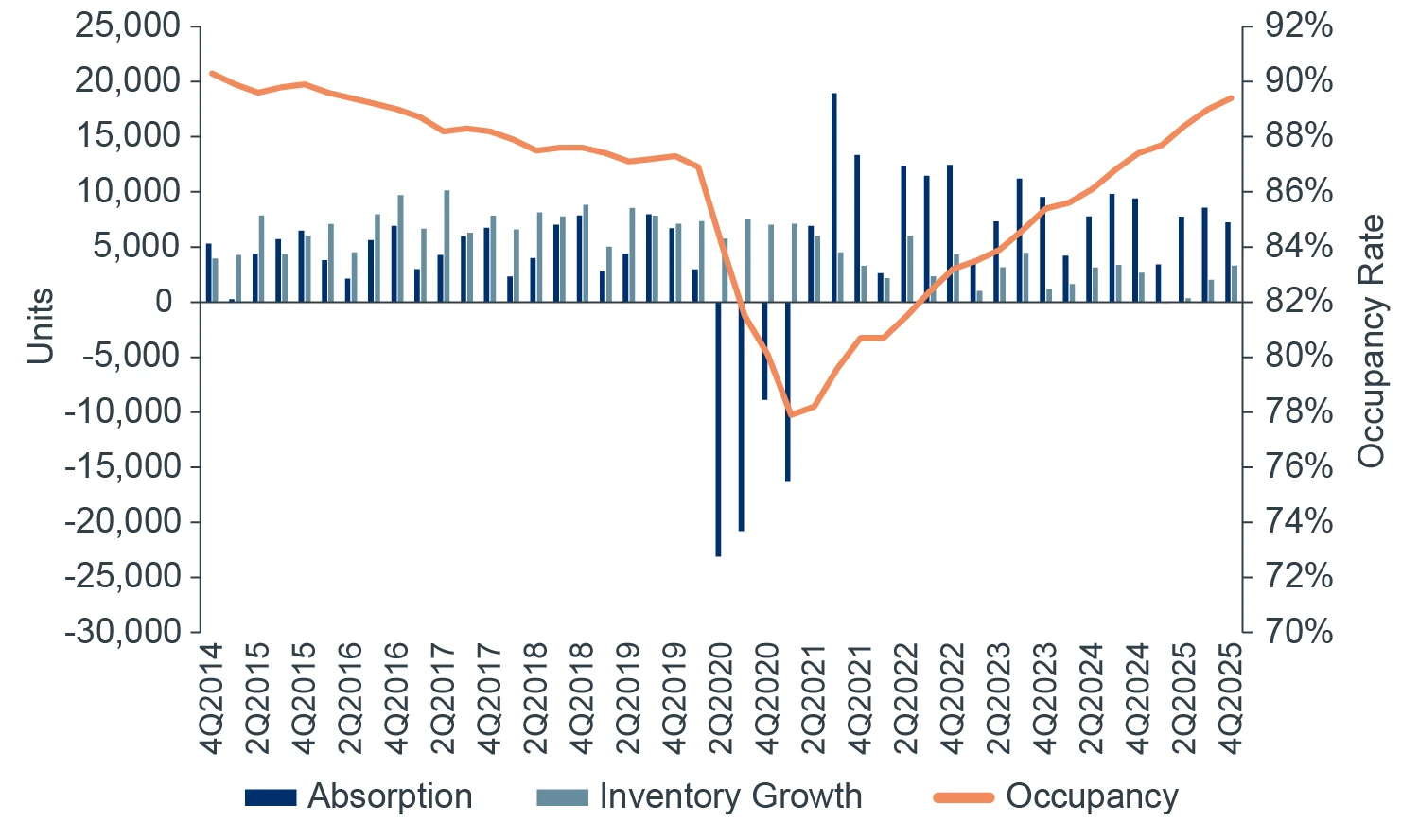

Supported by this demographic tailwind, senior housing fundamentals have recovered sharply, with occupancies reverting to pre-pandemic levels, and rent growth improving substantially (Figure 3). As of 4Q 2025, occupancy has risen to 89.4%, a 200 bps increase year over year and eleven percentage point increase from its pandemic low in 2021.3 Quarterly net absorption has averaged 8,800 units since 2Q 2021, two times the sector’s long-term historical average of 4,200 units per quarter.

FIGURE 3: BUOYED BY HISTORIC LEVELS OF NET ABSORPTION, OCCUPANCY HAS RECOVERED TO PRE-PANDEMIC LEVELS

Source: NIC MAP, as of 4Q 2025.

Despite the recent notable improvement in fundamentals, the supply response, thus far, has been extremely muted, with financing challenges and elevated costs and return requirements restricting senior housing construction starts. Senior housing starts have steadily declined in recent quarters, with total starts in 2025 slowing to 10,100 units, down 18% from the same period in 2024 and less than two-thirds of their most recent peak in 2021.4

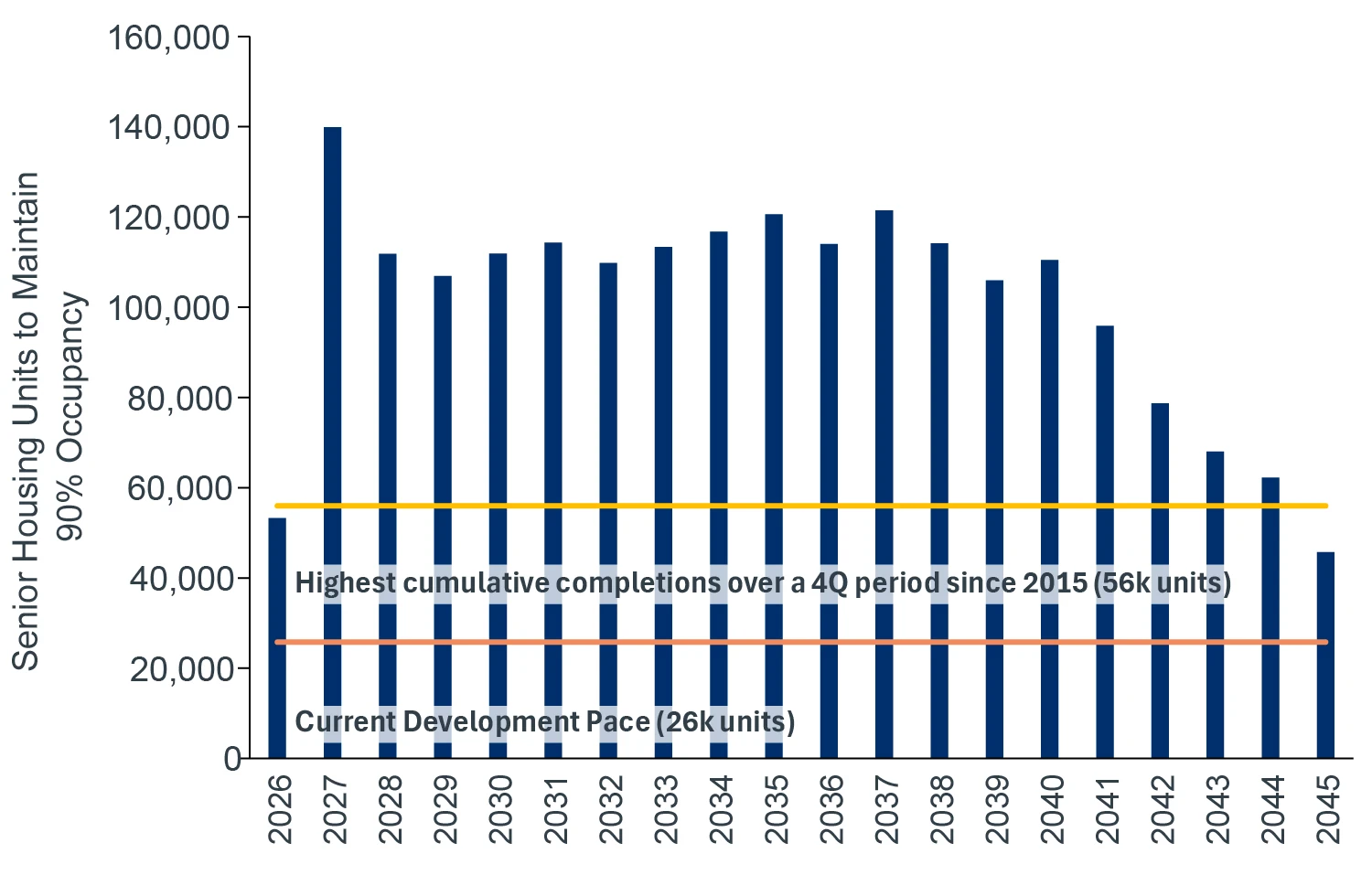

The diminished supply pipeline is expected to provide a meaningful tailwind for rents moving forward, as a significant supply/demand imbalance persists. Considering the impending surge in the 80+ population, the level of senior housing construction activity required to maintain market equilibrium (as measured by an occupancy rate of 90%), is significantly higher than both the current rate of building activity, as well as the highest rate of supply growth over a 12-month period at any point in the sector’s history5 (Figure 4). The rising and persistent demographic tailwind combined with a muted, near-term supply picture, should aid in maintaining favorable senior housing fundamentals and producing higher returns.

FIGURE 4: SENIOR HOUSING SUPPLY/DEMAND IMBALANCE

Source: Moody’s Analytics, forecast as of January 2026; NIC MAP, as of 4Q 2025; Clarion Partners Global Research.

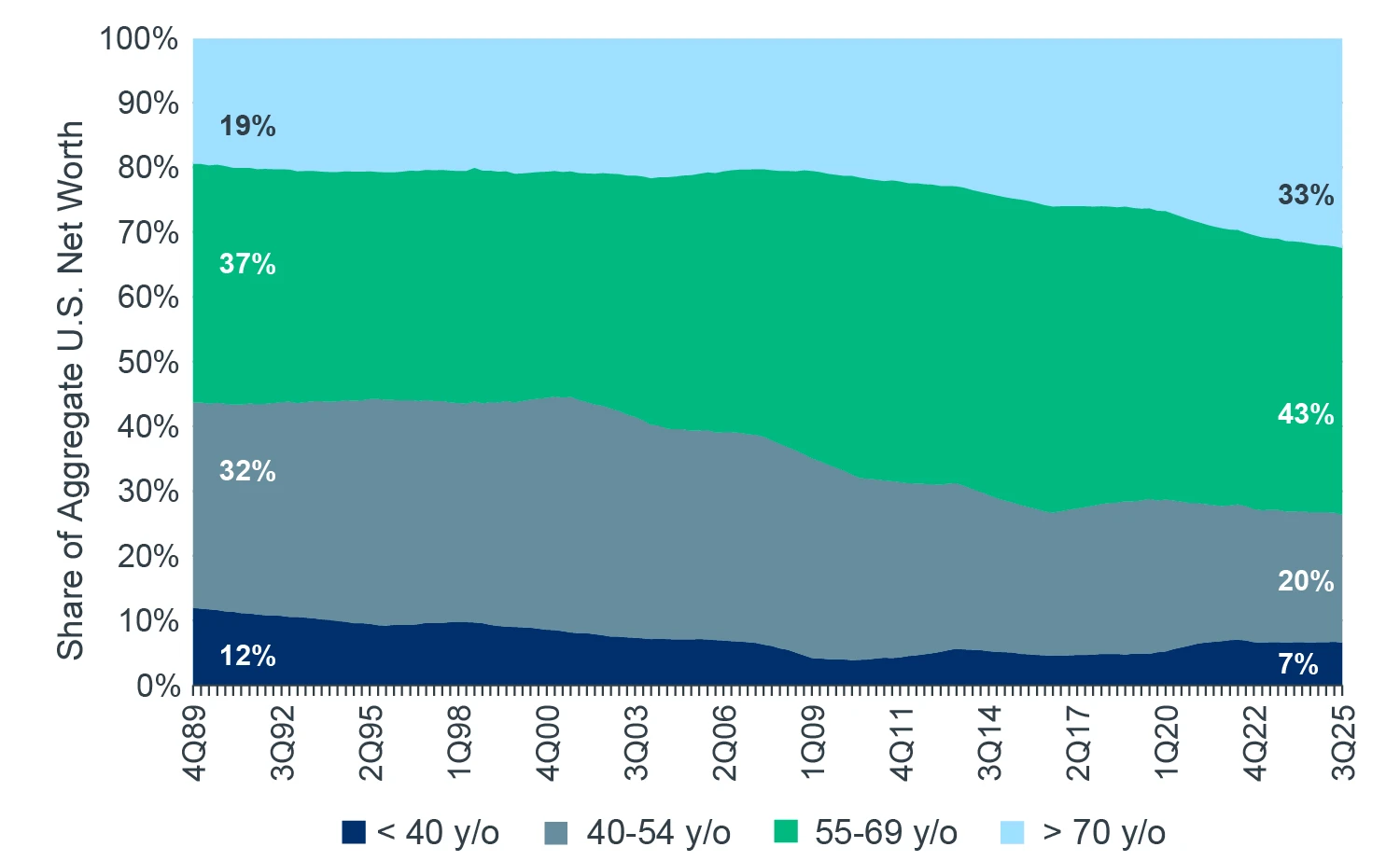

IMPROVED HEALTH & WEALTH SUPPORT RISING PENETRATION RATESIn addition to the sheer size and growth of the 80+ population cohort, today’s senior population is wealthier and living longer than senior populations from prior generations. Fueled by healthy home price and stock market appreciation in recent decades, aggregate household net worth nationally is increasingly concentrated among older households, with the growth in the median net worth for senior and adult children outpacing the increase in median net worth across all other age cohorts by a wide margin over the last few decades.6 The median net worth for the 75+ y/o age cohort was $334,700 as of 2022, 2x its inflation-adjusted median net worth in 1989 and the median net worth for the 65-74 y/o age cohort ($410,000) was highest among all age cohorts and was 2.3x higher than 1989 levels. In line with this trend, the concentration of household wealth nationally among 70+ y/o households has grown from just 19% in 1989 to 32% today (Figure 5), with investments in stocks/mutual funds and real estate accounting for 39% and 26% of this cohort’s assets, respectively.7 As a result, the health of the stock and housing markets are key determinants of senior housing affordability to residents. The improved wealth of seniors and their adult children should have a direct correlation to the uptake of senior housing and promote higher penetration rates.

FIGURE 5: U.S. WEALTH DISTRIBUTION BY AGE COHORT

Source: Federal Reserve, Distributional Financial Accounts - Distribution of Household Wealth in the U.S. since 1989, as of 3Q 2025.

Improving health outcomes among the aging population should also bolster senior housing demand. Mortality rates have trended downward over time, with increasing longevity and life expectancy across age cohorts. Life expectancies for males and females have risen to 76.2 years and 81.3 years, respectively as of 2019, up from 74.8 and 80 years in 2005.8 Shock mortality events, like COVID-19, had a disproportionate impact on the older population, producing a temporary dip in the increasing longevity trend. The long-term upward trend in longevity should continue, as medical advancements and new treatments contribute to increased life expectancy.

In addition to improved finances and health outcomes relative to prior generations, shifting family dynamics are likely to support increasing senior housing penetration. Adult children typically shoulder the responsibility of caregiving for aging parents. However, today’s smaller family sizes and changing family spatial proximity reduce the number of available caregivers within families, weakening a traditional safety net for the elderly. This trend is reflected in the steady decline in the percentage of the population aged 75 or older who live with other relatives (including adult children living at home), which has fallen to 26% in 2023 from an average of 33% in the 1980s and 42% in 1970s.9

OPPORTUNITIES

Acquisitions – Negative performance during COVID and financing pressure for recently-delivered projects with leasing challenges, coupled with increasingly strong fundamentals should continue to support a robust

acquisition pipeline and provide an attractive entry point into the market.

Development – The widening demand driven by the growth of the 80+ population has begun to materially exceed the growth of senior housing inventory. The resulting supply/demand imbalance has created the need for new capital and development in the sector. The development deficit created by the current pace of construction and the necessary number of units to keep up with unprecedented demand equates to a $275 billion investment opportunity by 2030.10

Financing – Stress on ownership and capitalization structures over the last decade from COVID, slow lease ups, and the change in the cost of financing also create an attractive opportunity for direct and mezzanine debt capital to provide interim solutions to owners.

Increasing Margins – The operating environment is improving supported by increased labor availability, which has led to moderating wage growth relative to the period in the immediate aftermath of the pandemic. Looking

forward, continued advancements in home health and patient monitoring technologies (e.g. remote health monitoring, social engagement) should help mitigate rising operating costs.

RISKS

- Rising Labor Costs/Availability – Despite improvement in labor costs (60% of total operating expenses) from pandemic-era levels, wages are poised to remain elevated over the next few years given the persistent shortage of health care workers and more stringent restrictions on immigration under the current administration. However, the strong historical correlation between labor cost and rent growth reflects the sector’s inelastic demand, as well as the ability of owners to pass through cost increases to tenants.

- Economic Downturn – Although demographic tailwinds are a prominent driver of demand, an economic correction could prompt a decline in asset valuations, particularly within public equities and real estate, negatively impacting older-household net worth, as well as the ability of adult-children to contribute to the cost of senior housing, contributing to lower senior housing affordability and penetration rates.

- Delayed Adoption – Continued technological advances and new home health services may allow aging residents to remain in their homes for longer than historical trends suggest, postponing an eventual move to senior housing. For senior housing operators, this could translate into shorter length-of-stays and an older and more dependent senior housing population, requiring the need for higher intensity care and increased staffing levels.

Against a backdrop of a compelling demographic tailwind and a muted, near-term supply outlook, senior housing market fundamentals are expected to remain healthy going forward. This favorable outlook is bolstered by stabilizing operating costs supported by improving labor availability and the continued adoption of innovative, patient-care technologies. The sector's recovery following a turbulent period in the immediate aftermath of COVID has generated an attractive entry point for investors. With all signs pointing to an influx of new investment into the sector, senior housing is poised to outperform.