Executive Summary

The convergence of long-term structural drivers and emerging cyclical tailwinds suggests the industrial sector may be approaching an inflection point, with conditions increasingly supportive of new development. For the industrial sector, development is a critical part of strategy, delivering modern, higher-throughput facilities that expand capacity, enable automation, and improve supply-chain efficiency, supporting tenant growth and long-term competitiveness.

- Cyclical signals:

- Supply constraints, including political issues, have created a near-term advantage for experienced, well-capitalized groups with fully entitled projects.

- Demand appears to be improving, with net absorption showing signs of recovery toward pre-pandemic levels.

- Big-box leasing activity, historically a leading indicator for broader market trends, is picking up.

- Structural tailwinds, including continued e-commerce growth, warehouse obsolescence, and ongoing supply chain modernization, underscore the need for modern logistics space within a tightening market.

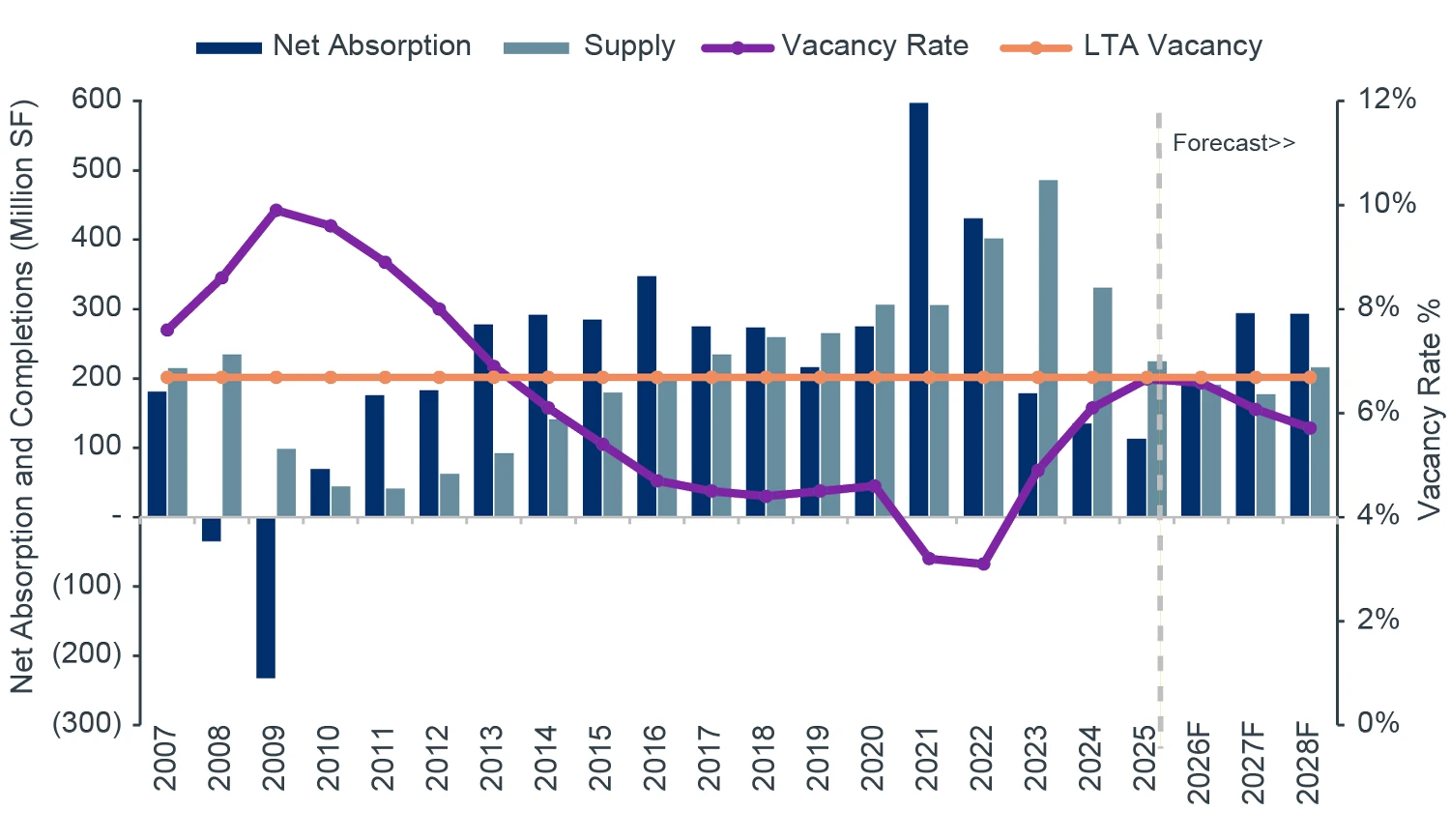

SUPPLY-DEMAND REBALANCING IS UNDERWAYThe supercharged growth of the pandemic era began to subside in 2023, and the U.S. industrial sector entered a period of space recalibration, or right-sizing, as demand cooled and capital constraints emerged. Increased policy volatility and geopolitical uncertainty provided an additional headwind to tenant activity, most notably with the “Liberation Day” announcement in April 2025. Industrial leasing activity fell below historic norms, with net absorption of less than 200 million square feet (MSF) annually from 2023 to 2025.

More recently, signs of improving demand are beginning to materialize, with the recent pickup in net absorption indicating that occupier demand is trending back toward levels last seen between 2015 and 2019.

Despite the recent slowdown, the U.S. industrial market has not sustained negative net absorption, and vacancy has remained at or below long-term averages, distinguishing the current environment from the more severe dislocation experienced during the Global Financial Crisis (GFC). As a result, the industrial sector enters this next phase with comparatively less excess slack to absorb.

After bottoming in 2025 (~113 MSF), net absorption is projected to reach equilibrium in 2026 before widening in 2027 and 2028 (Figure 1).

FIGURE 1: U.S. INDUSTRIAL FUNDAMENTALS

Source: CBRE-EA, Clarion Partners Global Research, 4Q 2025. Net absorption

is based on quarterly change in occupied stock using vacancy rate. Orange

line is LTA vacancy rate from 2002 to 2025. Forecasts have certain inherent

limitations and are based on complex calculations and formulas that contain

substantial subjectivity and should not be relied upon as being indicative of

future performance.

In addition, vacancy is stabilizing and even falling in some markets. Looking ahead, national vacancy is expected to decline modestly to a mid-6% range this year before falling below 6% in 2028.

As demand normalizes at sustainable levels, the market’s capacity gap becomes more apparent. With an aging, functionally obsolete stock base and a shrinking pipeline, new development is needed to meet next-cycle space requirements and the demand for more modern, efficient buildings.

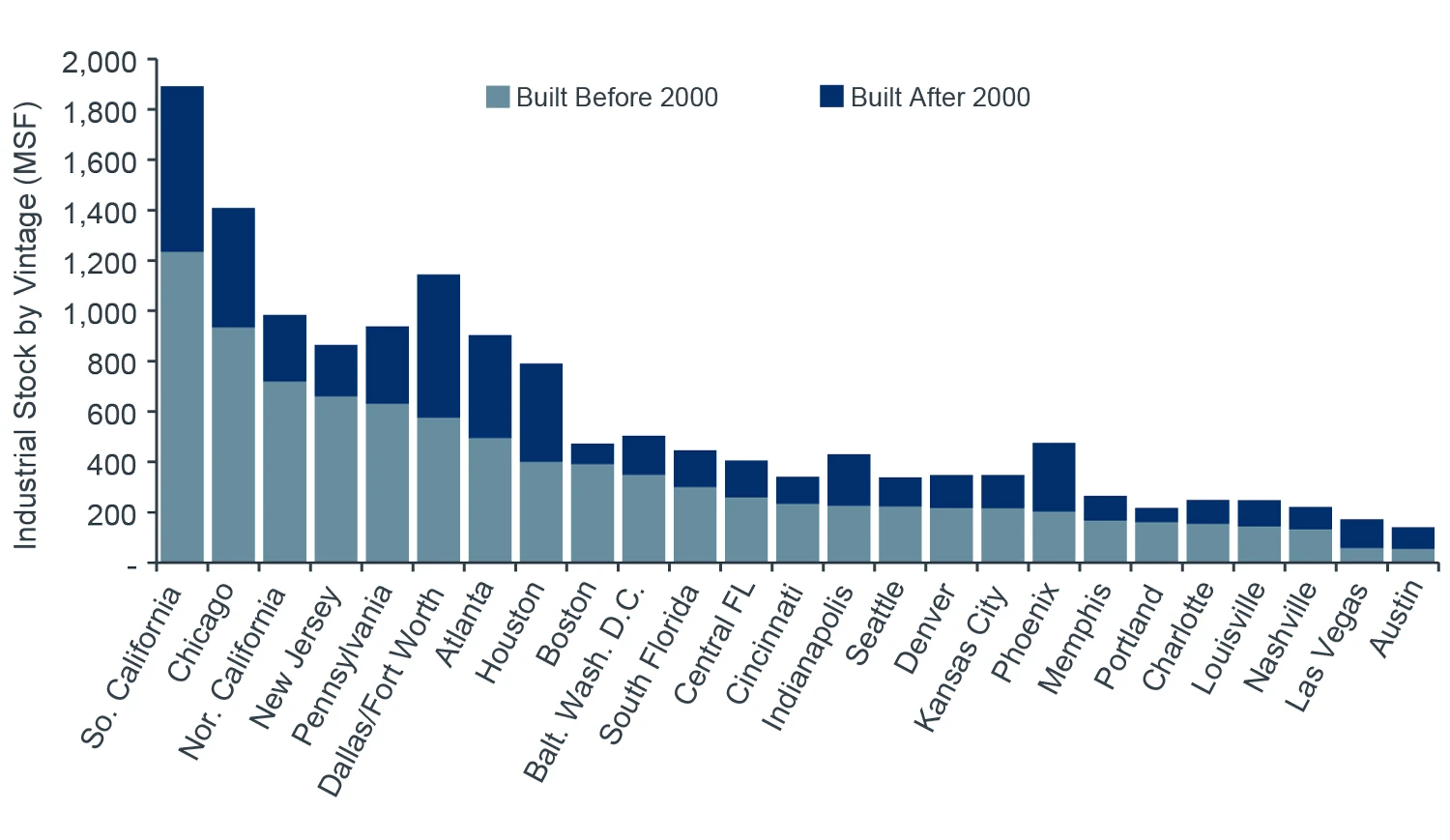

THE OBSOLESCENCE OPPORTUNITY: AGING STOCK AND THE NEED FOR MODERN FACILITIES

Modern tenant needs are materially different from much of the existing industrial inventory nationally, with 65% of square footage built prior to 2000 and 88% built prior to 2010. Nearly 10% is approaching or exceeds 50 years in age (Figure 2). Following robust development cycles in the 1980s and 1990s, the pace of new construction moderated in subsequent decades.

These older assets typically lack features in demand by tenants, including sufficient clear heights, dock door density, ESFR sprinkler systems, ample truck courts, and layouts capable of supporting automation and robotics. For example, they often have clear heights below 24 feet versus 32–40+ feet expected in modern facilities and significantly lower dock door ratios. In some cases, older buildings may also have insufficient power supply or less adaptable power configurations, which can constrain their ability to meet the operational and efficiency requirements of many tenants.

FIGURE 2: MAJORITY OF U.S. INDUSTRIAL STOCK IS

FUNCTIONALLY OUTDATED

Source: Clarion Partners Global Research 1Q 2026, CBRE-EA.

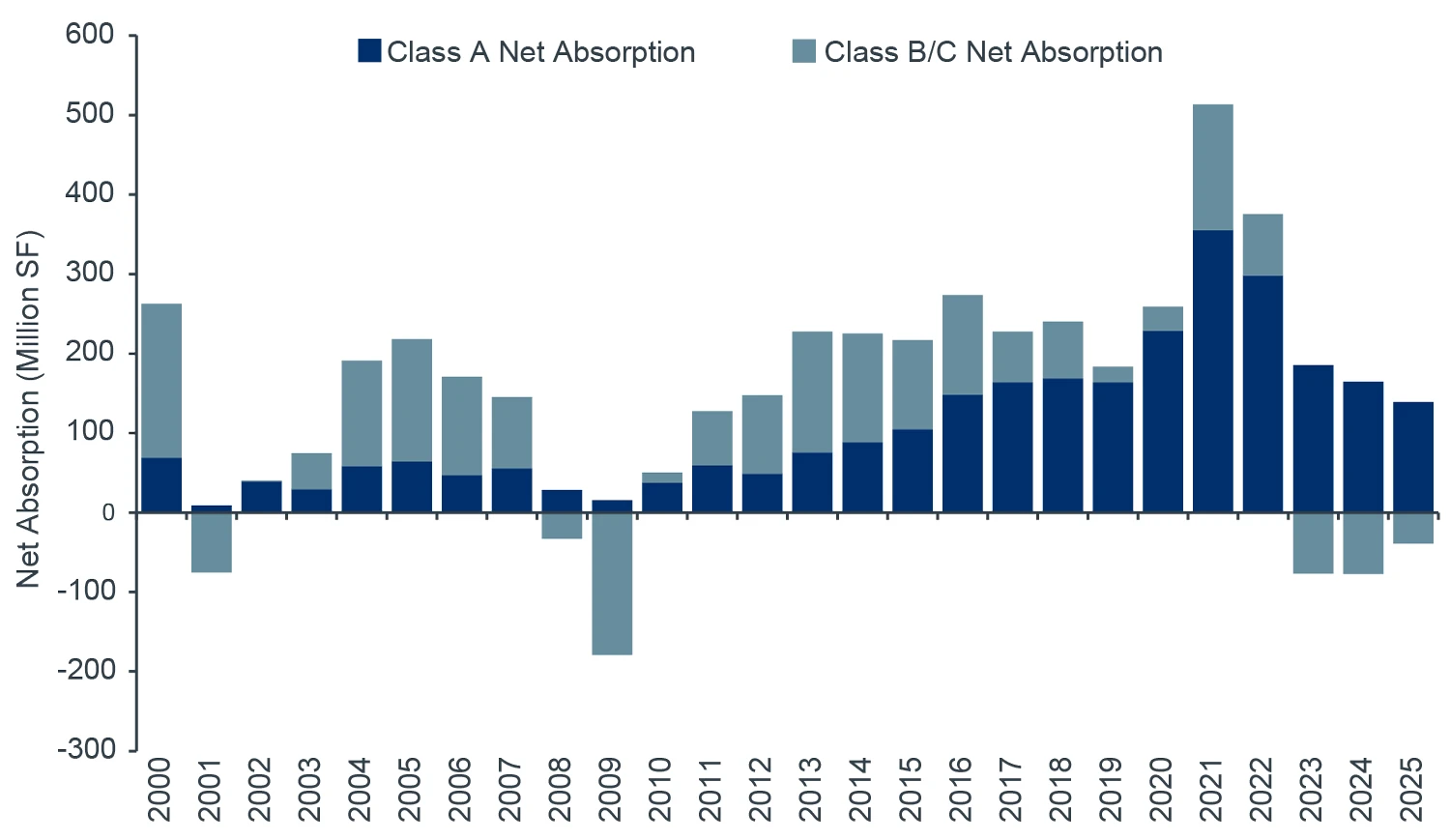

Consistent negative absorption (-217 MSF) over the past three years in Class B/C warehouse space reflects this weakening demand for functionally constrained structures, while demand remains strong for modern logistics facilities. Tenant preference for modern space has supported consistently positive Class A net absorption since 2000, even during periods of broader market slowdown. In fact, Class A assets accounted for 71% of warehouse net absorption since 2010. They also demonstrated notable resilience during the GFC and the recent market recalibration from 2023 through 2025 (Figure 3).

The market is increasingly differentiating between modern and functionally constrained vintage assets. Over the past decade, newer properties have seen asking rent growth 200 bps higher than older properties (8.6% versus 6.6%), have not experienced rent deceleration to the same degree, and command an approximately 20% rent premium on a PSF basis.1

The combination of modern tenant requirements and legacy inventory unable to meet those needs represents a durable structural driver underpinning the need for new industrial development.

FIGURE 3: TENANTS PRIORITIZE MODERN FUNCTIONALITY,

LOCATION AND EFFICIENCY

Source: CBRE-EA, Clarion Partners Global Research, 4Q 2025. Based on

warehouse product type.

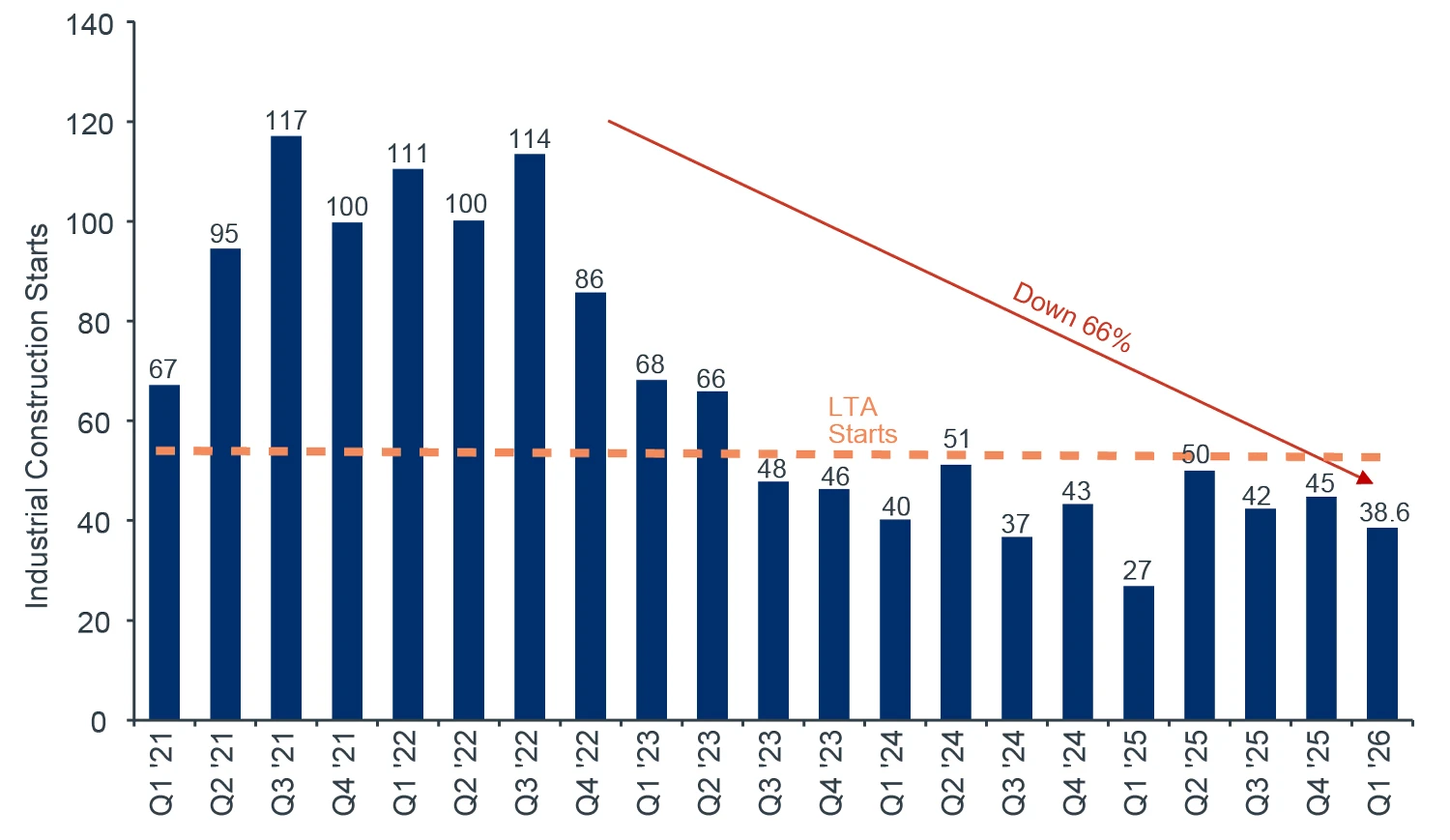

SUPPLY CONSTRAINTS REINFORCE TIMING

Despite strong underlying demand, the ability to deliver new industrial space is constrained by a range of structural frictions, including capital markets pressures (higher cost of debt, tighter lending standards), regulatory, physical, and economic hurdles, resulting in slower and more limited supply responses than headline pipelines suggest.

This headwind is further reflected in construction activity, with starts down sharply from peak levels (approximately 60% below the most recent quarterly peak) and now trending below the long-term average for 11 consecutive quarters (Figure 4).

FIGURE 4: U.S. CONSTRUCTION STARTS DOWN SHARPLY FROM

PEAK LEVELS

Source: CBRE-EA, CBRE, Clarion Partners Global Research, 1Q 2026.

Note: Past performance is not indicative of future results.

Regulatory and development friction have become significant barriers to entry. These include zoning limitations, heightened community opposition to new industrial development, competition with residential builds and data centers, development moratoriums and other growth restrictions in an increasing number of markets, as well as extended timelines for securing entitlements and permits.

Recent activity highlights the growing complexity of delivering new industrial supply. A growing number of municipalities have enacted moratoriums or imposed stricter limitations on new warehouse development, including Perris and Rialto, California; Mansfield, New Jersey; and Canal Winchester, Ohio. At the same time, historically pro-development markets, including portions of Dallas-Fort Worth, Nashville, and Atlanta, have become increasingly resistant to new industrial rezonings and entitlements. These trends reflect broader political and community concerns around industrial expansion, contributing to longer development timelines and increasing uncertainty around future supply delivery.

At the state level, California’s AB 98 legislation introduced additional design and siting requirements for logistics facilities, restricted truck routes, and increased the complexity of the entitlement and permitting process.2 These examples illustrate that regulatory friction is not confined to individual localities but rather reflects broader systemic tightening across major logistics hubs.

Additional challenges include the scarcity of well-located infill sites and competition with higher value uses, as well as infrastructure and design challenges, such as traffic mitigation requirements and insufficient utility capacity, particularly power.

While the development timeline for vertical construction of logistics facilities is relatively short compared to other property types, the overall development timeline can extend over multiple years when including site control and entitlement through to delivery, and some of these projects do not ultimately reach completion. Visible construction pipelines may overstate the volume of near-term deliverable supply.

These constraints are most pronounced in high-demand, infill, and coastal markets, where new supply is slower to materialize and more limited in scale. This dynamic creates meaningful timing considerations, as the delivery of development often lags shifts in demand and broader market conditions.

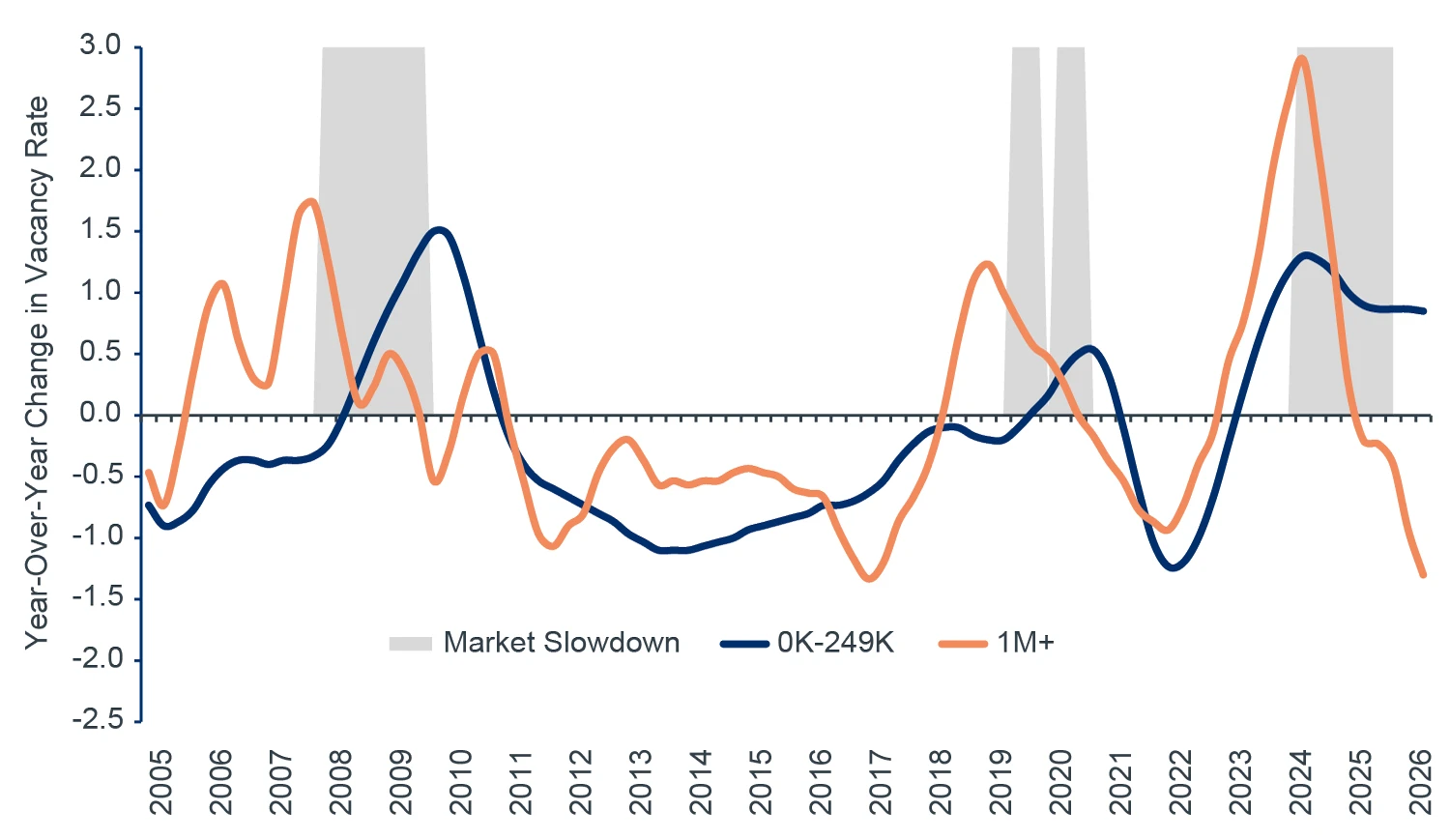

BIG BOXES: A LEADING INDICATOR OF STABILIZATION

There are increasing signs that leasing is stabilizing and demand is rising for new warehouses and distribution centers. Big-box, or large-format, modern distribution facilities are typically good indicators of what is expected to play out through the rest of the market. These facilities are often leased by national retailers, e-commerce operators, and third-party logistics providers.

Leasing decisions by big-box tenants are typically tied to national logistics networks and driven by long-term demand forecasting. Setting them apart from smaller, more regional tenants is access to large amounts of real-time sales data, inventory trends, and supply chain analytics, as well as a generally longer-term time horizon for new leasing decisions.

Because they are among the most-scaled, data-driven, and operationally sophisticated occupiers, they are typically the first to pause expansion, and the first to re-engage as conditions stabilize. They see demand shifts earlier than smaller tenants and are typically less reactive. This was evident in the recent slowdown when big-box leasing was the first to pull back, and it is now recovering earlier than the broader market.

Over the past several quarters, we have seen a reacceleration in leasing activity in the big-box segment, suggesting that larger occupiers are once again expanding footprints (Figure 5). This is expected, as this segment is also the primary beneficiary of long-term e-commerce growth and the growing preference for modern, high-throughput logistics facilities.

Given the segment’s historical role as a leading indicator, the recent rebound in big-box leasing activity may signal improving conditions for the broader industrial market.

FIGURE 5: U.S. LARGE TENANTS HISTORICALLY LEAD LEASING

RECOVERIES

Source: Clarion Partners Global Research, CBRE-EA, 1Q 2026. Gray

shading indicates economic / market slowdown (including net absorption

falling below average).

WHY SUPPLY MAY NOT CATCH UP QUICKLY

Development decisions are driven by forward-looking rent and yield-on-cost expectations, which can act as a limiting factor when current rents do not yet reflect improving fundamentals. In some markets, replacement rents exceed in-place rents.

Developers require sufficient rent levels to justify construction costs and execution risks. When a gap exists between market rents and required rents, projects are delayed and new starts remain muted. As a result, even as demand improves, supply does not immediately respond.

This is particularly the case as rent growth moderates and construction costs remain elevated, even if stabilizing. In some places, the feasibility gap remains and development is selective.For example, the gap between average market rents and replacement rents can be as high as 30% today, depending onsubmarket conditions and asset characteristics.

However, scale, expertise, and deep market knowledge can help identify opportunities even where headline market-level metrics may not suggest attractive development potential. As demand continues to recover and vacancy declines, market rents are expected to move toward replacement cost levels in a broader range of locations. This dynamic reflects a more typical cyclical adjustment process, whereby improving fundamentals help support development feasibility over time.

Taken together, this dynamic suggests that new development may remain constrained in the near term, even as fundamentals improve, allowing rents to reset toward levels that support future supply. For those developers with sites that pencil today, there may be an advantage to being an “early mover,” getting ahead of the next wave of larger scale development activity. Those projects are likely to face limited competition upon delivery.

Even so, if development remains constrained for too long, supply could become increasingly limited, with vacancy tightening to unsustainable levels over the long term. While that would be supportive of rent growth and existing asset performance, it could also reduce market fluidity and hinder occupier expansion, reinforcing the need for new supply. At the same time, the timing and pace of this recovery remain subject to broader economic and geopolitical risks.

While the outlook for new industrial development remains constructive, the sector is not immune to near-term risks. Changes in trade policy, including tariffs, could increase costs and uncertainty across supply chains, causing businesses to delay investment and expansion plans. Geopolitical tensions could also weigh on growth, resulting in higher prices domestically, which would impact not only consumers and industrial occupiers, but also many of the inputs for new construction.

In such scenarios, the recovery in industrial market fundamentals may be more protracted than expected. However, we believe several factors are currently helping to temper these risks, including historically balanced vacancy levels, a reduction in new construction activity, and continued demand for newer, high-quality industrial facilities.

CONCLUSION

As we look ahead, four key takeaways continue to support our outlook:

- Demand is normalizing and beginning to reaccelerate, led by big-box leasing.

- The existing inventory base is aging and increasingly misaligned with modern tenant requirements, creating durable replacement demand.

- The supply response is structurally constrained by entitlements, land scarcity, infrastructure, and capital, with starts already sharply lower.

- Initiating well-located projects during today’s quieter window can position new product to deliver into the next period of tightening, supporting both occupier needs and risk-adjusted returns.

Well-capitalized, experienced groups holding entitled land sites are positioned to translate these themes into advantage. As big-box demand recovers, they can use data from their own portfolios as well as relationships with tenants and brokers to underwrite with better information, structure pre-leasing or phased delivery, and target submarkets where network optimization is driving the next wave of absorption. The obsolescence gap creates an opportunity to deliver “right-spec” product, with higher clear heights, trailer/storage ratios, enhanced power, and automation-ready layouts.

In a supply-constrained environment, and over the long term more generally, experience navigating entitlements, community processes, and infrastructure requirements becomes a competitive moat, while scale supports tighter procurement, standardized designs, and stronger control of schedule and cost. Finally, with long development lead times and starts down, well-capitalized groups can secure sites or leverage existing land banks, advance entitlements during the current lull, structure capital to withstand lease-up volatility, and deliver into a potentially tighter market with less competing new supply.